Five things to consider about Alphabet (Google)

Google is now trading at a decade-low Price to Earnings (P/E) and confidence in the company being a long-term stock pick winner is growing rapidly. I recently added Alphabet (GOOGL) to my portfolio as well, but with the stock recently becoming a lot more accessible to new investors, following their 20-to-1 stock split and the hype reaching new levels, I wanted to share some of my own long-term considerations. I hope this might also give some insight into the holistic approach I myself practice when I consider the full value and future positioning of a business beyond the numbers.

1. Concentration risk

Google commands an incredible market share in Online Search. But with this, combined with being a relatively young company for its size (founded in 1998) also comes concentration risk. Google is heavily reliant on advertising revenue, making up the vast majority of its revenue and profits.

Credit to Genuine Impact for this nice visualization of data.

80% of Google’s revenue comes from advertising according to their latest financial numbers. $39.6 billion of the $69.7 billion comes from advertising revenue inside its own search engine, but even its second and third largest sources of revenue come from serving ads, being YouTube (Video Streaming) and Google Network (Ads provided outside of their own services). Needless to say, a large part of the company’s profits are tied to this, which is a risk to consider, particularly as signs point to a slowing economy. Advertising usually does best in a growing economy, where people are much more willing to spend and it will likely be the number one thing for investors to keep an eye on in upcoming quarters.

2. Competition through new ways of interaction

Google made a ground-breaking investment back in 2006 when it acquired YouTube. Considering that they bought it for $1.65 billion back then and how it now brings in $7.3 billion in revenue, it is safe to say it is doing well. I am an avid user of the platform myself and adore it in many ways, but I am not convinced of its success in the future. Google has spent years strategically pushing creators on the platform to create longer-form content in an effort to maximize each video’s profitability. According to YouTube’s monetization policy, mid-roll ads are only able to be placed in videos exceeding 10 minutes long, driving many creators to strive for this benchmark. As a viewer, you may even have noticed this too. It has worked well in the short term and helped grow YouTube into the revenue-generating asset that it is today, but suddenly shorter-form content poses a threat.

The popularity of short-form content is easily exemplified by the meteoric rise of TikTok but is seen elsewhere too, with Snap (SNAP) popularizing 'Stories' on social media, then followed by Instagram and Facebook, and yes, even YouTube as well (Shorts). This type of content is now so in demand that Meta (META), the owner of Instagram and Facebook is releasing a revamped interface that puts their TikTok-like 'Reels' front and center for the first time. But short-term video content is not just a threat to Google's video streaming business, but to their Search business as well. Nearly half of Generation Z is using TikTok and Instagram for search over Google, according to the company's own data. And to me, this makes sense: If you want to look up a quick recipe or tutorial, this type of content usually works much better for that. There could even be an argument that it offers much more genuine insights into what you might be looking for, than what you will find on the front page of Google.com among paid results - and I do not think YouTube's half-assed implementation of Shorts solves any of this.

My family & I recently visited a small town in Northern Mallorca, Spain - and in preparation for the trip, my girlfriend searched TikTok and found a place to go horseback riding, which we ended up doing as a result, seeming like a great way to experience the area.

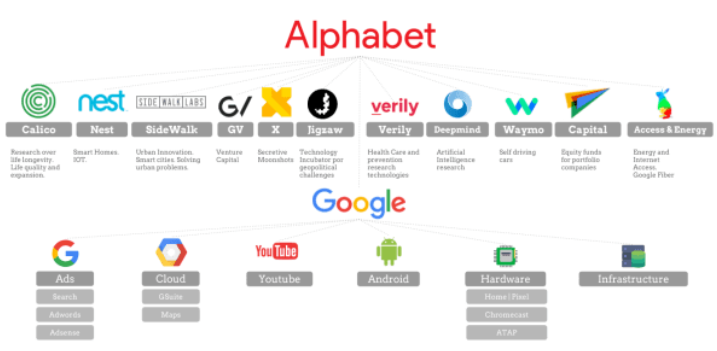

3. Failure to find success in 'Other Bets'

Part of Google’s business is known as ‘Other Bets’. This is where the company invests in new ventures like its self-driving project Waymo and its internet services like Google Fiber. Many exciting projects come to live under this umbrella – and many come to die. The list of failed projects is long and even in its core operations, Google is notorious for shutting down projects and lacking focus. One could argue that Google has not made successful acquisitions since they bought Android in 2005 or YouTube in 2006 – long before the ‘Other Bets’ business unit was even established. Google bought Motorola in 2012 for $12.5 billion but sold it again, just two years later, to Lenovo (0992) for $2.91 billion – Granted they did probably extract lots of value from this deal, before letting go of it (including some patents still used today). Likewise, I was sad to see Google let go of Boston Dynamics in 2017, a well-known robotics maker, for reportedly a mere $100 million.

Boston Dynamics serves as a good example of the kind of innovative investments I really wish Google would hang onto, considering their unique position to fund such interesting endeavors. My mind boggles with ways I can see this type of tech changing the landscape one day. Of course, it remains to be seen if Google’s ‘Other Bets’ are to work out – Many projects are in their infancy and may one day become the next big thing. Waymo certainly stands a chance of changing the world one day, as I consider this the leading self-driving project right now, only behind Tesla (TSLA).

4. Company structure

Tied to all of the above is the issue of the way the business is structured. In 2015, Google restructured and introduced its parent company Alphabet, which now owns all parts of its business under its umbrella. This remains a little-known fact, at least outside of the investing circle, and that alone serves as clear evidence that it has not yet quite worked out the way they wanted it to. Google, with its concentrated advertising business, makes up almost the entirety of its operations, profit-wise.

Alphabet now consists of many different operations, but chances are you know very few of the non-Google ones.

However, I am glad this strategy shift has been made already, as I believe it to be a potential life-saver when it comes to dealing with regulatory scrutiny and against being perceived as a monopoly in the public eye – Being forced to split up has long been a threat to Google. But if they are to score any real points in this aspect, they need to succeed somewhere outside of their core brand and focus on creating that perception change. One way they could show they are serious about making this change would be if they changed their stock ticker, much like what Facebook did after its name change to Meta. I talked a bit more about this in my Metaverse post.

Speaking of stock tickers, I find it inconvenient and unnecessarily confusing that management insists on having the company split into several public-facing tickers. Class A shares are called GOOGL and offer voting rights, while Class C shares are called GOOG and offer none. As you might guess, Class B shares exist as well but are thankfully only for insiders. To my knowledge Alphabet is the only large tech corporation utilizing a share structure like this. It makes Alphabet stock a little harder to include in market cap-weighted Index funds or quickly calculate its core valuation numbers as an investor. I wish they had announced some change to this alongside the stock split, in an effort to make the stock even more accessible for retail investors. It really is not a big deal, but again hints at management’s failure to portray their business most favorably, in my opinion.

In the iShares MSCI World ETF, which aims to weigh companies by market cap, the list has to represent Alphabet twice, because of their share structure, which offers confusion.

5. The missing dividend

My final point mostly comes down to personal preference. Even as an investor in technology trends and disruption I have really grown to appreciate the consistency and ongoing reward that is dividends. Particularly in times like these with the markets under pressure – it is a great thing not to be forced to sell in order to make a profit on your shares. Alphabet is at this point, such a large and healthy business that it should start issuing a dividend. Microsoft (MSFT) and Apple (AAPL) have both done so for years and have been great at steadily increasing it over time from a relatively low bar. Many would probably argue that they as a growing company, are better off just reinvesting into their business. However, I say that the track record of their non-Google ventures suggests otherwise. After all, they are already among the top 5 most valuable companies in the world, so to me, it is about time. Many funds will not even consider purchasing shares of a non-dividend paying company and I believe it also helps create long-term investor loyalty and reason to stick around.

The Bottom Line

All in all Alphabet (or just Google?) is an immensely profitable business and I too believe in its long-term success. They command a massive market share above 90% of Online Search which positions their business as one with a massive moat. But after 20 years, this very well-protected castle is starting to show some cracks, with platform competitors and short format content providers like TikTok and Instagram appealing more to next-generation internet users than just plain text web results. This is worth being aware of before considering buying (more) of the stock. However, I still believe Alphabet to be a quality business, currently trading at a fair value. I see a huge opportunity going forward with Google’s excellence in Artificial Intelligence and Machine Learning – making the vast amounts of data they have access to so much more valuable.

Google AI unintentionally took the spotlight recently after one of their (now-ex) employees claimed their LaMDA project to have become sentient. A true testament to the level of advancements of this potentially redefining part of their business. I highly recommend the read.

While I generally think highly of Sundar Pichai, the company’s CEO, I do question general management’s ability to best serve investors’ interests through pursuing the right investments internally. In May of this year, I finally took the plunge and made Alphabet a small part of my portfolio. In truth, I wish Google had long been part of my portfolio as it is just the kind of business I really like and understand as I happen to be entirely dependent on many of their services every single day. I will not rule out the possibility of adding more shares over time, however, if it is to stay in my portfolio permanently, it needs to soon start issuing a dividend or succeed outside of its core brand of Google. This though raises the question for me of how they aim to do this, while still making it easy to use all of their services under one unified account.

Disclaimer: I am not a financial advisor, the opinions expressed in this article are entirely my own – always invest at your own risk.