Apr 2023 - Earnings and a surge in Energy

April has come and gone. Another dull month in the world of finance... Well, sort of. Unless you're one of those who gets a thrill out of major companies absolutely smashing earnings expectations and a regulatory shutdown of the biggest gaming deal in history.

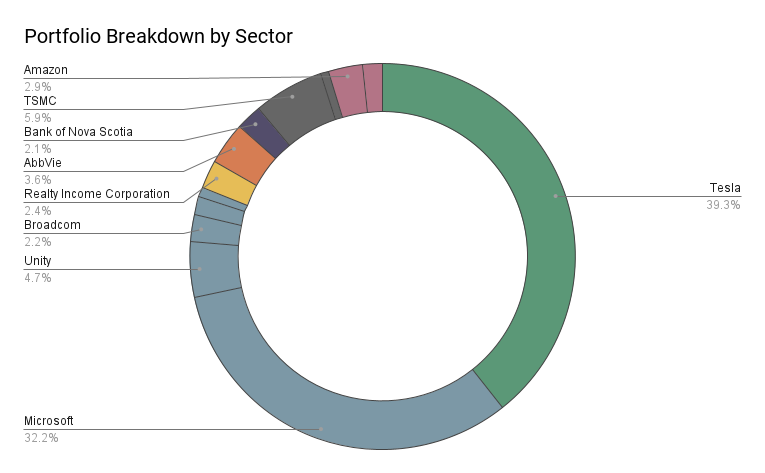

Overview

Unlabeled on the chart:

In Consumer: Starbucks (1.6%)

In Industrials/Manufacturing: 3M (0.7%)

In Technology: Adobe (0.8%) and Alphabet (1.5%)

Moves

No active moves were made this month.

Performance

My portfolio value decreased by 9.72% in the month of April, significantly trailing global markets keeping mostly flat over the same time period.

Dividend overview

| Name (Ticker) | Received | Amount (USD) |

| Broadcom (AVGO) | Apr 4th | $23.29 |

| Taiwan Semiconductor Manufacturing Company (TSM) | Apr 17th | $44.98 |

| Realty Income (O) | Apr 17th | $13.98 |

| Bank of Nova Scotia (BNS) | Apr 27th | $45.00 |

| Total | Apr 2023 | $127.25 |

I received a total of $127.25 in dividends before taxes for April 2023, a significant increase of 39.12% over the same month last year at $91.47.

Commentary & Review

Out of the game, already?

Just a few days ago, Microsoft’s (MSFT) $69 billion acquisition of Activision Blizzard was put on pause by UK regulators in a somewhat unexpected move. While a deal of this magnitude is unlikely to slip by regulators unchallenged, this one has turned out more rollercoaster-like than many had expected. It was not long ago that both US and EU regulators attempted to put a stop to the deal, echoing concerns shared by Microsoft’s competition in gaming (mainly Sony (SONY)). But these concerns were swiftly alleviated as Microsoft smartly negotiated 10-year licensing deals with all competing platforms…. Except for Sony. But while the US and EU seemed content with other game distributors securing access to Call of Duty for the decade, the UK is citing other concerns. Interestingly, the UK is specifically targeting Microsoft for their Cloud Gaming efforts - one area of the business which I am particularly excited about. There is no doubt about it: Microsoft is vastly in the lead in this important industry (of the future), but here is the kicker: It is not because of anti-competitive practices, but rather due to others’ incompetence. Alphabet (GOOGL) famously threw in the towel on their game streaming service Stadia at the beginning of this year - less than three years after it launched. Nvidia (NVDA) seems unable to grow its offer, under the chosen strategy of licensing every game from publishers and Sony’s PlayStation Now is a downright embarrassment (Speaking from first-party experience).

Because of this, I would argue that UK regulators are making a mistake. Because of Microsoft’s shown commitment to this acquisition, I believe they can with a few simple changes in language to their negotiated licensing deals, easily avoid these concerns. I also believe that gaming is, in general, much less of a threat to individual consumers, should competition concentrate. As I have shared a few times already, I am a strong believer that this deal will eventually go through. I had planned on trying a short-term trade with Activision but initially missed out on it. Now, after a 10% drop in share price due to this decision, this possibility is back on the table for me.

My expectations for Unity going into Q1 earnings.

Before I get to the really interesting earnings stuff, let me just get some other gaming-related (ish) news out of the way first. Unity (U) this month, launched “Unity Industry” an optimized offering for building/construction enterprises to utilize RT3D. While not major news, it is still exciting as I continue to see the company I am now so heavily invested in, make the right moves in alignment with my thesis. While Unity is by many simply considered a game engine, its potential lies at least equally outside of gaming, with practical real-life use cases like this one. Some have asked me how I expect Unity to make it out of Q1 earnings. To this, I have answered that I set my hopes to end up right in line with expectations or slightly above them. I expect Unity to generate their second-ever profitable quarter on a non-GAAP basis - which might still take some analysts by surprise as there seems still to be some yet to account for the positive effect ironSource will have for the company’s EPS. That said, there is nothing that interests me greater in relation to Unity earnings than management commentary on the earnings call. I hope to hear strong, continued efforts to reduce stock-based compensation rates, as this issue overshadows all else. Profits on a non-GAAP basis are not fooling anyone when the contrast to GAAP earnings is this large. But I do expect easing inflation and interest rate hikes to work in favor of Unity this time around. I am really excited, actually.

Big Tech smashing earnings

Tesla (TSLA) started this earnings season off with a mere “pass”, as numbers came in right in line with expectations. Despite this, the stock reacted very negatively the following day. But long-term investors should rejoice. While vehicle margins have been suppressed as Tesla has slashed prices on all their models in the past couple of months, they are still industry-leading. The shareholder deck also included imagery of the Cybertruck production line, as the company once again reiterated that production should start by the end of Q3 in spite of naysayers. But as you know, while I am a big fan of Tesla as a vehicle maker, success for my long-term thesis depends on their ability to scale their Energy business into significance. And this is where it gets fun: Energy deployed increased 360% YoY this quarter, while revenue of this segment jumped 148%. As I have also discussed before, Tesla seems finally ready to fully commit their efforts to Energy - which is long awaited. I believe this is the start of an exponential growth curve for Energy, much like we saw with vehicle sales with the release of the Model 3.

“Unlimited power!”

To help others understand why Tesla slashing vehicle pricing is not a sign of rising competition or demand concern, this month I also shared a thread to Twitter explaining how the notion of Tesla as a PREMIUM vehicle maker is plain wrong and how this misunderstanding can lead to completely missing the bigger picture.

TSMC (TSM), Amazon (AMZN), Alphabet, and Microsoft all three truly crushed their earnings. While Microsoft was the only one fairly rewarded for this effort, with shares jumping 8% the following day, I think it is worth giving credit where credit is due. TSMC had guided for weakness this quarter but managed to slightly beat still-high expectations. Q2 is likely to be another tough quarter for them, but there is little doubt for me that TSMC will manage to outperform every other player in the industry, foundry or not. As you might expect, I also really like it when my major holdings decide to collaborate: While still unofficial (rumors) news, it seems Microsoft is relying on TSMC to build their own custom AI chips. In one of my first posts on this site, I outlined how many cloud providers like Microsoft and Amazon were working on building their own chips to support efficiency. This is seemingly happening now with this project codenamed Athena, built on TSMC’s 5nm process. This is not only doubly beneficial for me, but also just great news for the industry.

“Everything is proceeding exactly as I have foreseen.”

Amazon shares rose 11% in after-market trading, as numbers came in much higher than expected. But as CEO Andy Jassy shared expectations for slowing cloud growth, this reaction was immediately reversed. The only real disappointment to come out of Amazon’s earnings for me was the little to no mention of the technologies they innovate for in physical retail. Alphabet also managed to beat expectations slightly, despite continued resistance in advertising. While the stock was likewise punished by something the CEO said on the call, about how they approach AI, Google managed to demonstrate their first-ever profitable quarter for their cloud offering. Once again, I believe this is reason for rejoicing among long-term investors, although I would agree, that so far, Google’s reaction to Microsoft’s AI march of war, has been weak. Finally, Microsoft is doing well, as always, with their biggest hit to profits seemingly coming from foreign exchange conversion. The news about Activision once more being put on hold interestingly came out the day following earnings but did not seem to scare off investors. The only place where Microsoft is really struggling right now is in hardware, which could indicate short-term troubles for former arch-enemy Apple (AAPL) and other hardware makers like Nvidia. It certainly has roughed up Samsung (5930) just a little.

Even Meta (META) posted a massive earnings beat. It seems all is well for now. So, now all there is left is to wait for Unity and some of my other favored holdings like Starbucks (SBUX) to deliver on their earnings. I apologize for glossing over earnings for my more conservative holdings like AbbVie (ABBV) and 3M (MMM) but my assessment is for those, that things are as they have been for the past couple of months. AbbVie is working hard to make up for its fading core patent through new revenue streams and 3M continues to struggle under ungodly lawsuits and has initiated another round of mass layoffs. More on my Twitter for those interested.

Watch List

My Watch List sorts stock by sector and notes are included for each one, describing my interest and reservations. The status indicates the likelihood of a position being added to my portfolio. ‘Watching’ means I just keep an eye on them, whereas ‘Top Pick’ means they are very likely to find their way into my portfolio at one point - ‘Under consideration' means somewhere in between, with notes offering some elaborating thoughts. Please note my Watch List is based on my own research and goals and is in no way a recommendation of what to buy.

| Sector | Name (Ticker) | Status | Notes |

|---|---|---|---|

| Healthcare | Novo Nordisk (NOVO-B) | Top Pick | Strong innovator, previously owned, familiar |

| ARK Genomic Revolution ETF (ARKG) | Under consideration | Considering as an alternative for CRSP | |

| Merck & Co (MRK) | Watching | Casual interest, limited familiarity | |

| Medtronic (MDT) | Watching | Casual interest, limited familiarity, attractive dividend | |

| Industrials/Manufacturing | A.P. Møller - Mærsk (MAERSK-B) | Watching | Lacks ambition in electrification efforts |

| Elkem (ELK) | Top Pick | Too expensive, great positioning | |

| Otis (OTIS) | Under consideration | Potential dividend growth play, familiar | |

| Norsk Hydro (NHY) | Watching | Casual interest, limited familiarity, attractive dividend | |

| Lockheed Martin (LMT) | Watching | Ethical concerns, too expensive | |

| Corning (CLW) | Watching | Weakening moat, rising competition, familiar | |

| Consumer | McDonalds (MCD) | Watching | Strong brand, limited optionality |

| LVMH Moët Hennessy Louis Vuitton (MOH) | Under consideration | Strong leadership, performance, too expensive | |

| Costco (COST) | Top Pick | Incredible moat, leadership, too expensive | |

| Coca-Cola (KO) | Under consideration | Strong brand, stable giant, too concentrated, familiar | |

| PepsiCo (PEP) | Under consideration | Strong brand, well diversified, familiar | |

| Hasbro (HAS) | Watching | Strong product line, shaky mangement | |

| Energy/Utilities | Ørsted (ORSTED) | Top Pick | Strong positioning, leadership, familiar |

| Waste Management (WM) | Under consideration | Stable giant, limited familiarity | |

| NextEra energy (NEE) | Watching | Strong position, too concentrated, too expensive | |

| Enphase Energy (ENPH) | Watching | Rising star, limited familiarity, too expensive | |

| Technology | Embracer (EMBRAC-B) | Under consideration | Incredible acquisitions, not profitable, familiar |

| Sea (SE) | Watching | Core business weakening, innovator, just turned profitable | |

| Activision Blizzard (ATVI) | Top Pick | High conviction that MS acquisition offer will go through | |

| Palantir (PLTR) | Watching | Amazing tech, highly dilutive, unprofitable, opaque | |

| Meta (META) | Watching | Strong leadership and userbase, undergoing big change | |

| Apple (AAPL) | Watching | Strong brand, loyal userbase, risk of disruption | |

| Mercado Libre (MELI) | Watching | Great execution, growing market, too expensive | |

| Squarespace (SQSP) | Watching | Familiar, too concentrated, too expensive | |

| Shopify (SHOP) | Watching | Innovator, well positioned, unprofitable | |

| Xiaomi (1810) | Watching | Fast innovator, China risk, previously owned | |

| Nvidia (NVDA) | Watching | Strong brand and leadership, too expensive, previously owned | |

| Finance | Coinbase (COIN) | Under consideration | Strong brand and leadership, unprofitable, previously owned |

| BlackRock (BLK) | Under consideration | Strong execution, exposed to the economy, attractive dividend | |

| Whitehorse Finance (WHF) | Watching | Attractive dividend, strong execution, high risk | |

| Sofi Technologies (SOFI) | Watching | Strong leadership, innovator, unprofitable | |

| JP Morgan Chase (JP) | Watching | Stable giant, overlapping industry with holding | |

| Manulife Financial (MFC) | Watching | Stable giant, attractive dividend, limited familiarity | |

| Real Estate | VICI Properties (VICI) | Top Pick | Strong leadership and execution, attractive dividend, too concentrated |

| Digital Realty (DLR) | Watching | Good positioning, attractive dividend, limited familiarity |

Disclaimer: I am not a financial advisor, the opinions expressed in this article are entirely my own – always invest at your own risk.