Why I am not selling: Tesla

I became a shareholder of Tesla (TSLA) in April 2016 and I consider that one of the single best decisions I ever made in my life. I remember returning home from a month-long trip to Seattle with a new perspective on the popularity of their cars. As I was looking for a new long-term opportunity after unexpectedly exiting a position in Intel (INTC) Tesla is where I settled. Inspired by their mission toward a greener future, their leadership, and their tech-focused approach Tesla became my third-ever long-term investment after Microsoft (MSFT) and Novo Nordisk (NOVO B).

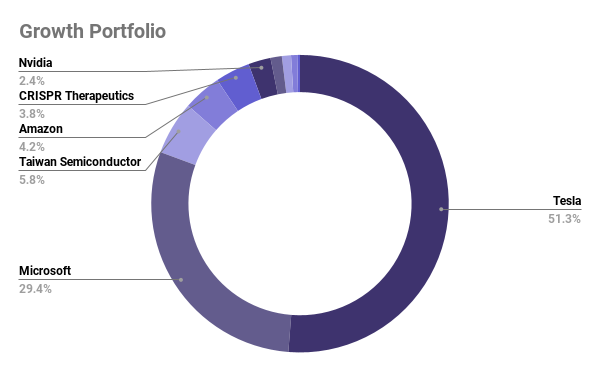

Today Tesla makes up more than 50% of my entire portfolio, in part attributed to me buying more shares in March and again in November of 2019 - but more significantly so because of the 1150% return I am currently sitting on with this investment. My confidence in this company is strong and despite all the noise I see in mainstream media and in the online investing communities I visit, I remain extremely bullish on the future of the stock and plan not to sell any time soon.

My growth portfolio as of late July 2021.

Holding TSLA makes you grow a thick skin

One reason for how I am able to sit through all the criticism, FUD, and misinformation out there about this stock is that I have been through all the ups and downs imaginable since holding in the past 5 years. Maybe now more prominently than ever the company CEO Elon Musk is under scrutiny from the public for his activity on Twitter. Most recently an outspoken part of the crypto community rallied against him as Tesla reversed their decision on accepting Bitcoin as payment for their cars. He has used his platform to speak out against unions and try to downplay the seriousness of the pandemic. Even more concerning, back in 2018 he shook the market and brought the stock to a halt with this infamous tweet:

I remember reading that tweet with mixed feelings: Excited for my investment to have definitely paid off yet disappointed that I would likely no longer be able to stay part of this company's incredible future growth story. But as we know it today, it never became a reality and instead, it landed Musk in trouble with the SEC and ultimately cost him the role as chairman of the company along with a multi-million dollar fine.

When I check the investor community page for the stock on my online brokerage I see a strip of comments criticizing the company: Comments from Musk that have not quite been delivered on yet1, supposed falling demand and sales statistics2, car fires3, and endless technical analysis revealing an evaluation that is out of this world4. None of this phases me. Each of that criticism can be tackled quickly and easily - so easily in fact that I have done it in the footnotes at the bottom of this post.

At the same time, exactly this is part of what makes this company so interesting: It commands an incredible amount of interest, publicity, and discussion. More than any other stock I have ever owned. What this company is doing is so unbelievable that it seems like pure imagination to some. It is hard to grasp the concept of exponential growth and in analyzing this kind of stock you have got to look further out than just a few quarters - Which seems against the norm on Wall Street. But the long-term sentiment speaks for itself - The future is electric and Tesla is in the lead. By more than just a mile.

More than just a car company

This phrase gets thrown around a lot but it is not without merit. Today the vast majority of Tesla's revenue and profits come from its vehicles. However, since its acquisition of SolarCity back in 2016 the company has been serious about its ambitions in renewable energy production and storage. One of the products that hold the most potential yet have been struggling to meet expectations is the Tesla Solar Roof. One of the coolest concepts I have ever seen announced and a dream come true for someone like me: Blending practicality and aesthetics, with solar panels to make up the individual roof tiles, ultimately creating a seamless product that is nearly indistinguishable from the real thing. I remember a story getting me really excited for the first installations of this product in my country of Denmark, but ever since then I have heard nothing of it here.

Tesla Solar Roof was unveiled in 2016, a few months after the acquisition of SolarCity.

Production has proven more difficult than imagined with bad yields and various other challenges. Installations have been slow and messy, sometimes very expensive. Demand for the roof seems to be high, yet Tesla is unable to quite deliver on this. A few promises have also not made the cut: Currently, only a single skew is available to order, whereas originally the product came in a few different variants and styles. To tackle the issue of demand, Tesla this year decided to bundle all new orders for Tesla Solar with their own battery solution - it is all or nothing from now on. On the flip side, Tesla's residential battery solution called Powerwall is doing really well for the company - Still struggling to meet demand however as the majority of batteries are being allocated for their vehicles. Tesla has also made strides with their enterprise battery solutions 'Megapack' and 'Powerpack' powering Apple's new California-based solar farm and back in 2017 when they built the biggest battery in the world in just 90 days to help stabilize the power grid in Southern Australia.

A render of the Tesla Megapack, though the real thing does exist!

Part of what justifies Tesla's evaluation is its energy business. The energy sector consists of companies with a much larger market cap than those of the auto sector. In fact, many of the largest companies in the world are within the energy sector, although many today are of course in oil and gas. Renewable energy companies are set to take their place within the next couple of decades and I believe Tesla to be among the top contenders. With all this said and done, it would still be fair to criticize Tesla's evaluation as of today based on the hope that their energy business might one day turn into a large revenue stream for the company. But more remains to be taken into account.

These kinds of charts are often used to put Tesla's evaluation into a negative light. Source: thedrive.com

One reason that the auto sector usually does not see the biggest valuations is that traditional vehicle production is a low-margin business. Based on numbers from 2019 - GM grossed approximately 18% on its automotive business - a company that sells more than 10 million cars annually. In comparison, Tesla grosses nearly 30% already which is around 3 times the industry average and Tesla is yet to produce even 1 million cars in a full year. Now how is this possible? Out of all the companies on the chart above Tesla is the only one producing 100% electric vehicles. EVs are much simpler machines in comparison with traditional ICE vehicles and so it is much easier to profit from. Right now the most expensive part of an electric car is the battery and here Tesla is in a prime position by having by far the most efficient batteries on the market. In comparison, the Tesla Model 3 costs the same as a Ford F-150, yet has over 12% more range with a battery of 54 kWh whereas the Ford uses a 125 kWh battery. Looking at the long-range models the difference is even starker. Tesla's early commitment and now incredible lead is paying off big time and is part of what makes their future so profitable.

Artificial intelligence and Tesla's self-driving future

Another topic that comes up a lot when discussing Tesla's evaluation is its potential in self-driving cars. While their cars technically are classified as level 2 today they are already approaching level 3 in many aspects. And so are many of their competitors. The big difference, however, lies in the data: Tesla started collecting driving data on all their vehicles back in 2017 through the autopilot program and this is now giving the company a major long-term advantage. By the latest numbers from 2020, the company has collected data from more than 3 billion miles driven. This gives Tesla the possibility to train its AI models much more confidently and much more true to life. As an example, GM's Cruise self-driving program is often spoken very highly of by investors and seen by many as more capable than Tesla's. However, it only works in a limited sandbox environment and is not quite yet ready to be set free in any location or in any situation, unlike Tesla's Full Self Driving beta.

While this software is still far from perfect, it does inspire confidence in me to see how it can now be used to such a degree all over the American continent and how it overcomes challenges in countless difficult situations. FSD is able to stop for red lights and does so with a comfortable roll, it navigates various cityscapes and it works on the highway. It often times deals well with construction zones, roundabouts, and crosses with bad visibility. Even more impressively and importantly contributed to the vast amount of data Tesla has: It relies entirely on camera vision. All of Tesla's competitors in the self-driving space make use of LIDAR, a bulky and still expensive sensor that measures depth using lasers. Musk has long been outspoken about the cost and design disadvantages of LIDAR and based on this took the more difficult road of relying entirely on the vision from the get-go. This has likely meant that it took the company longer than expected to get to its current stage of autonomy capability, but will pay off from here as they have displayed these impressive capabilities without it. Recently Tesla even went so far as to remove radar from their new vehicles - a move that has been up for much debate and required the company to rewrite tons of code. But again, it has proven successful and the company has managed to skip another cost and improve its margins further.

Ultimately self-driving cars will lead to what has been teased and talked about over the years: Tesla's self-driving fleet. A network of robo-taxis operating much like the likes of Uber (UBER) and Lyft (LYFT) though with the major advantage of cutting the biggest expense: The driver. Tesla has talked about making this feature available to all Tesla owners, giving an option in the app to let your car roam the streets and make money for you while do not need it. Studies have shown that the average car is parked around 95% of the time - so obviously there is a lot of room here for better utilization. It would also help offset the waste of resources used for personal transport vehicles in comparison to public transport solutions like buses or trains. Plans for this future fleet of autonomous became painfully obvious with the release of the Tesla Model 3 when Tesla transitioned to using a smartphone as the primary key instead of a fob along with the integration of an in-cabin camera so that the owner could potentially access evidence if something inside the car was damaged on one of its tours. With the smartphone app, Tesla is also working to integrate your personal preferences, so that no matter which Tesla you sit in, it will adjust music volume, air condition, seat height, and such exactly to your liking.

Some of these enhancements for future self-driving have made the Model 3 a popular option for existing taxi operators in Denmark today.

Importantly and often overlooked when talking about AI in the context of Tesla is its potential outside of self-driving. Tesla's in-house supercomputer is named 'Dojo' and boasts impressive capabilities. It is as of now mainly used for training self-driving models and algorithms based on the data collected from the 8 cameras that pride the majority of each of their vehicles. However, Dojo is expected to be able to do much more than that and its power could potentially be contracted out to outside clients. While much mystery surrounds this topic, we should soon know more as Tesla is hosting their first ever 'AI Day' on August 19, 2021. Here Tesla is expected to announce a new chip design as well as something exciting related to robotics. It really could be anything and as of now, we simply do not know. It has been made clear however that this event is focused entirely on recruiting talent in this field. Another interesting tidbit to know about this company is how a 2020 survey revealed that for engineering students their top choice for employment would be either one of Musk's two companies: Tesla or SpaceX.

The email invite for AI Day features an image showcasing this interesting new chip design.

So... Will I ever sell?

The short answer is: It depends. Some people are speculating that Tesla may one day offer a dividend. If that turns out to be the case I will likely never find a good reason to really sell if the company's vision also continues to be carried out. I am myself very skeptical of this scenario and I do not see it happening for a long time - in which case I might already have sold. Some argue that once Tesla's self driving fleet is live along with the amount of vehicles produced and delivered at that point, the company will have more money than they would know what to do with. 'Solving The Money Problem' breaks down the possibility of Tesla dividends in this video and though most points seem valid, I remain skeptical of this scenario.

Should this not play out there will one day be a time I will sell. But only very little. My first and biggest reason is of course what I have tried to describe in this post: I still have a high conviction in this company and its potential to grow. That reason alone is enough for me to stay, even though I have already made large gains. 2 years ago I started selling out my second biggest investment. Microsoft, although I have really only done so to optimize my profits against taxes and to find new ventures to invest in. However, I still own a good chunk of Microsoft in my portfolio and because it is paying out dividends it is unlikely that I will see myself selling out completely.

Another reason is the situation I am in right now. In September of last year, I began university and I am lucky to find myself in a country offering not only free education but also a service called 'SU' - essentially a small salary handed to you by the government while you study, there are restrictions in place to stop me from taking such large profits from my investments, without having lost out on this benefit. This is by all means completely fair, but as I do keep a job on this side of my studies, the gap to hit the limit is even smaller. That means there is a zero percent chance I will sell a significant chunk of my Tesla stock for at least the next 2 years while I work on my Bachelor’s degree - and even longer if I should continue on a Masters.

Interestingly, when I made my first investment into Tesla back in 2016, I had a little dream of one day being able to purchase a Tesla car with the profits from that move. That is now entirely possible for me, even accounting for the taxes I would have to pay on taking profits, although I refrain from doing so a little longer. Maybe I have just become old and too rational in my thinking, but at the very least I would prioritize owning a home with space for an electric car to charge before I spring for such a luxurious option. Today I live in an apartment building that does offer a great parking space but not a single electric car charger to speak of. Although that has not stopped several of my neighbors from getting a Tesla...

One of three Tesla Model 3s currently visible from my apartment balcony.

Disclaimer: I am not a financial advisor, the opinions expressed in this article are entirely my own – always invest at your own risk.

Footnotes

Musk is super transparent. More so than most other CEOs. While he might not always deliver on his optimistic timelines, he ultimately does deliver. Musk has done the impossible several times around and always comes out ahead. The Tesla Model 3 and SpaceX's reusable rockets are direct proof of that. The track record is solid.

Tesla is losing market share. That is if you are looking at electric vehicle sales only. It is simple math really: Before no competition existed and now there are some. Yet quarter by quarter Tesla deliveries go up and their share of the total vehicle market goes up with it.

Electric car fires are much less common than ICE vehicle fires. Tesla accidents and fires are reported on unproportionally more often by mainstream media creating a skewed image of the facts. To combat the misinformation surrounding this topic, Tesla has dedicated a section on their Vehicle Safety Report site to fire statistics. You are almost 11x as likely to witness a fire in any other vehicle brand in comparison with Tesla.

TSLA's P/E ratio is incredibly high sitting currently at 384,62 - 20x the industry standard. Yet P/E is not a very good indicator of a company in this stage of growth, still growing more than 50% annually. Last quarter the P/E sat at 650 and last year we were looking at 1000. A lot of future growth is factored into the price, but as long as Tesla continues to grow at its currently forecasted pace, it is entirely justified.